Les actions préférentielles américaines ont chuté au premier trimestre de 2023, dans un contexte d'inquiétudes des investisseurs quant à la liquidité des dépôts de plusieurs banques régionales américaines (Silicon Valley Bank, Signature Bank, First Republic Bank) et du Crédit Suisse, une importante banque suisse. Bien que disposant de capitaux propres suffisants par rapport aux normes réglementaires, ces banques n'ont pas pu faire face aux demandes de liquidités liées à une panique bancaire classique, et les autorités réglementaires ont négocié leur rachat forcé par des banques plus solides.

Pour les déposants américains, les pertes latentes sur les portefeuilles d'investissement et de prêts ont constitué la principale source de préoccupation à l'origine de la fuite des dépôts. Ces pertes latentes étaient presque entièrement dues à la hausse des taux d'intérêt, qui a fait baisser le prix des bons du Trésor américain et des titres assimilés, lesquels représentent l'essentiel des portefeuilles d'investissement des banques. Les déséquilibres actifs-passifs les plus importants ont été propres à certaines banques et, selon nous, ne constituent pas une menace pour le système bancaire mondial dans son ensemble, qui compte 5 000 membres.

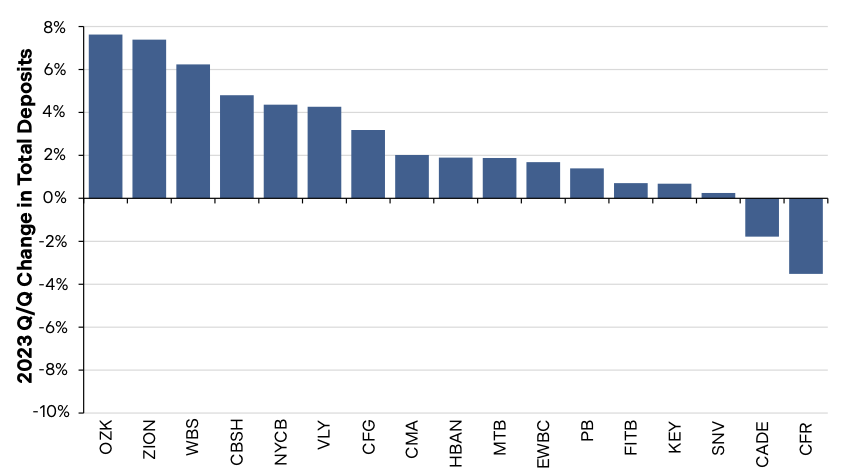

Les résultats du deuxième trimestre de 2023, publiés en juillet, étaient conformes aux attentes des analystes. Les ratios de capitaux propres sont restés solides et les banques régionales, en particulier, ont généralement réussi à attirer et à fidéliser les dépôts. Les dépôts non rémunérés ont diminué, remplacés dans la plupart des cas par des dépôts rémunérés, plus coûteux et constituant une source de financement bancaire plus coûteuse. Les investisseurs ont été globalement rassurés par les résultats du deuxième trimestre et les actions des banques américaines ont connu une légère hausse après la saison des résultats.

Croissance des dépôts des banques régionales américaines

Les banques américaines sont les principaux émetteurs de titres privilégiés américains, mais d'autres secteurs d'activité en émettent également, et les fondamentaux semblent globalement solides. Historiquement, les émetteurs des secteurs de l'assurance, des pipelines, des télécommunications et des services publics ont toujours été plus stables, et leurs émissions d'actions privilégiées contribuent à la stabilité et à la diversification d'un portefeuille d'actions privilégiées américaines.

Alors que les banques mondiales regagnent progressivement la confiance des investisseurs et que d'autres segments du marché se portent bien, voici quatre raisons pour lesquelles les investisseurs devraient envisager d'initier ou de renforcer une position en actions privilégiées américaines dès maintenant :

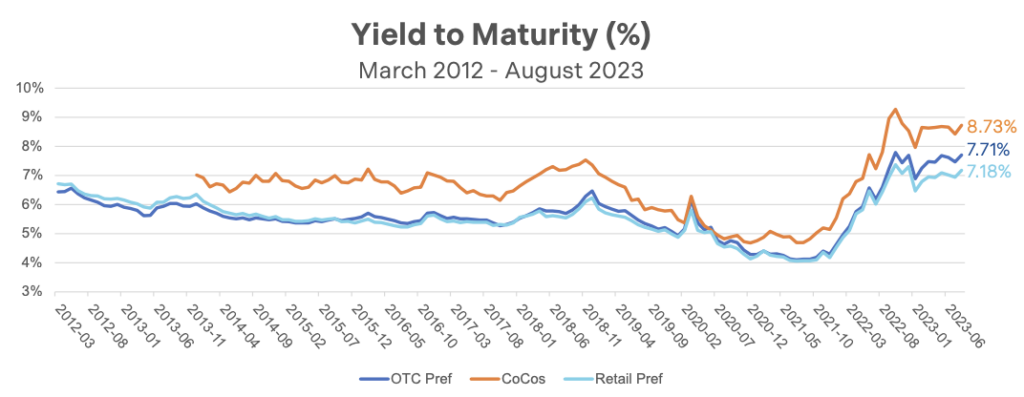

1) Les rendements sont attrayants et augmentent en raison des réinitialisations des taux flottants.

Les nouvelles émissions obligataires réalisées depuis le début de 2023 sont plus dynamiques qu'en 2022, et les taux d'intérêt se sont améliorés. Les banques américaines ont émis des obligations à court terme (AT1) avec des taux d'intérêt compris entre 6,25 % et 7,625 %, tandis que les émissions AT1 des émetteurs internationaux se situaient entre 7,50 % et 8,50 %. Les écarts sur les échéances secondaires (ou « back-end ») sont demeurés globalement dans une fourchette de 300 à 400 points de base, ce qui est considéré comme attrayant par rapport aux indicateurs de crédit de la plupart des émetteurs.

L'exposition de BPRF et BEPR aux obligations préférentielles à taux variable a également été un atout majeur pour le portefeuille au cours des douze derniers mois. Avec la hausse des taux d'intérêt observée au cours des dix-huit derniers mois, ces titres se sont classés parmi les plus performants. La plupart d'entre eux appliquent des formules de réinitialisation basées sur une marge par rapport au LIBOR à trois mois (largement remplacé par le SOFR), qui a progressé parallèlement aux hausses de taux de la Fed.

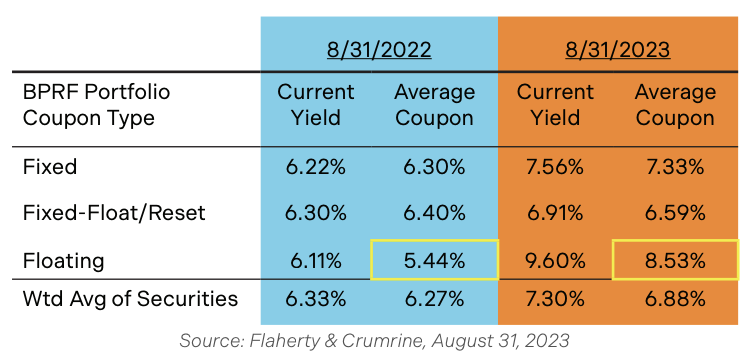

L'impact des révisions des taux d'intérêt sur le portefeuille a été significatif. Le taux d'intérêt moyen variable du portefeuille a augmenté au cours de la dernière année, passant de 5,44 % au 31 août 2022 à 8,53 % au 31 août 2023 (voir le tableau ci-dessus). Ces révisions plus élevées, conjuguées au réinvestissement dans de nouvelles émissions à taux d'intérêt plus élevés, ont fait passer le taux d'intérêt moyen de l'ensemble du portefeuille de 6,27 % à 6,88 % sur la même période.

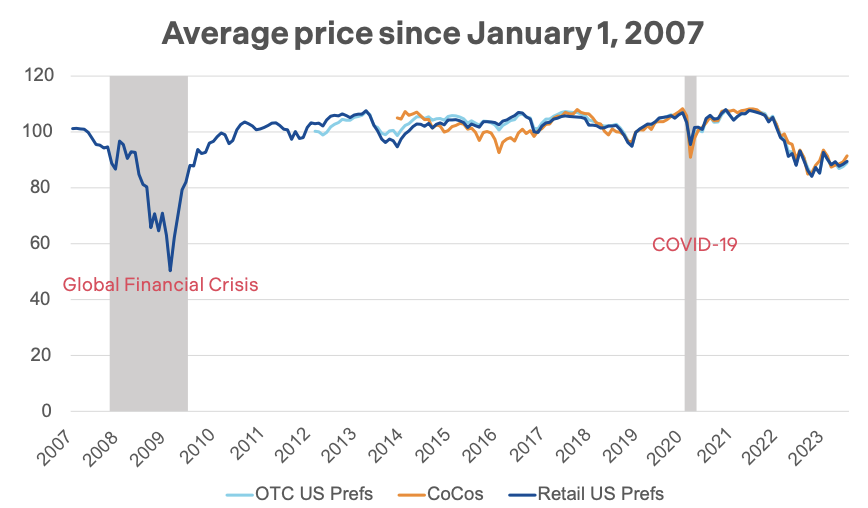

2) Les actions privilégiées se négocient avec des rabais intéressants par rapport à leur valeur nominale.

Les actions privilégiées américaines se négocient actuellement à rabais par rapport à leur valeur nominale jamais vue depuis la crise financière mondiale, certains segments étant même cotés à seulement 88 cents pour un dollar. Ces actions se négocient généralement près de leur valeur nominale et peuvent se vendre avec une prime. Les rabais actuels représentent une occasion potentielle d'appréciation substantielle du capital pour les investisseurs lorsque les taux d'intérêt finiront par baisser.

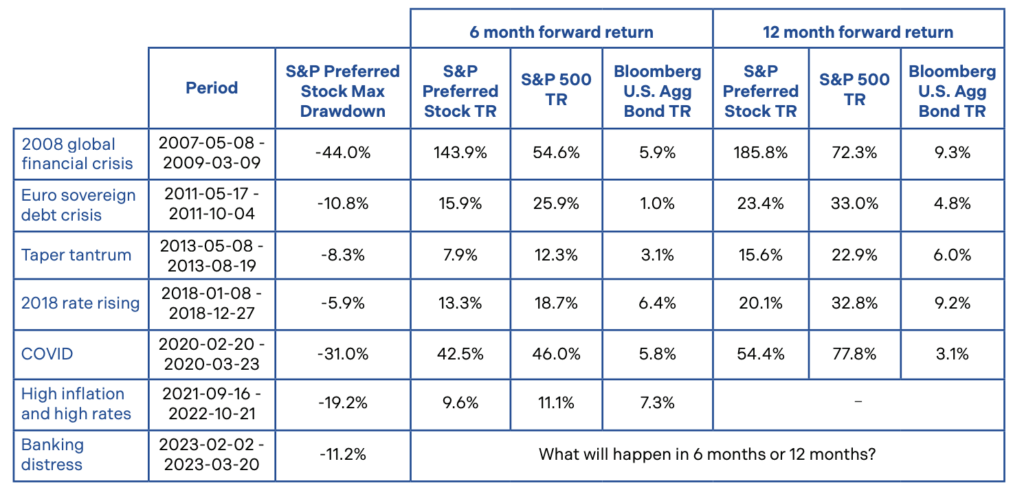

3) Historiquement, les actions privilégiées ont offert leurs meilleurs rendements lors des périodes suivant une correction du marché.

Dans bien des cas, les rendements observés après une correction de marché ont été à deux chiffres. Les actions privilégiées demeurant à des niveaux bas, il est encore opportun d'en profiter.

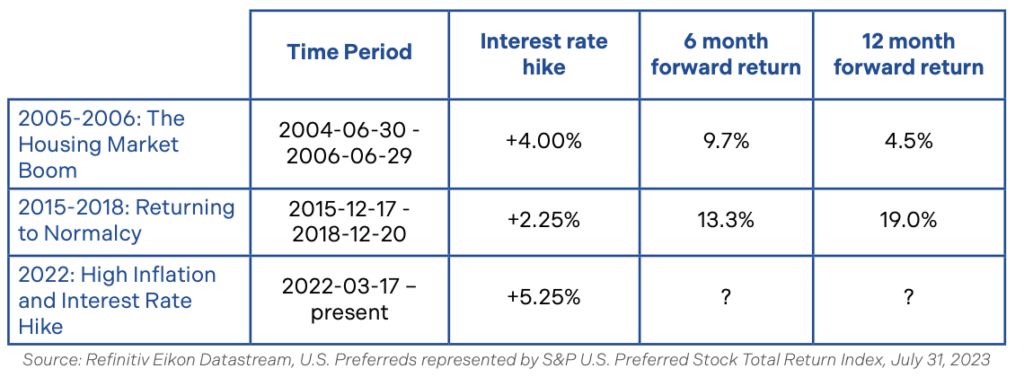

4) Les obligations privilégiées américaines ont affiché une solide performance après la fin des cycles de hausse des taux d'intérêt précédents

On ne peut pas dire avec certitude que la Réserve fédérale américaine ait complété son cycle de hausse des taux d'intérêt. Toutefois, les acteurs du marché estiment que si la Fed n'a pas terminé, elle est sur le point de le faire. Historiquement, les actions préférentielles américaines affichent de solides performances après la fin d'une ronde de hausse des taux d'intérêt.

Les marchés obligataires, y compris celui des obligations privilégiées, ont connu des difficultés au cours des 18 derniers mois, dans un contexte de hausse historique des taux d'intérêt. Nous croyons que cette situation offre aux investisseurs des obligations privilégiées américaines avec des coupons attrayants et des perspectives de gains en capital dans les périodes à venir.

L'approche de Brompton :

FNB privilégié de premier ordre Flaherty & Crumrine Brompton (BPRF, BPRF.U) et FNB privilégié de premier ordre amélioré Flaherty & Crumrine Brompton (BEPR, BEPR.U) offrent des moyens d'investir sur le marché américain des actions privilégiées avec l'avantage d'une gestion active par le spécialiste américain des actions privilégiées le plus ancien, Flaherty & Crumrine Incorporated.

Ce document est fourni à titre informatif seulement et ne constitue ni une offre de vente ni une sollicitation d'achat des titres mentionnés. Les opinions exprimées dans ce rapport sont celles de Brompton Funds Limited (« BFL ») et peuvent être modifiées sans préavis. BFL met tout en œuvre pour que les informations proviennent de sources jugées fiables et exactes. Toutefois, BFL décline toute responsabilité en cas de pertes ou de dommages, directs ou indirects, résultant de l'utilisation de ces informations. BFL n'est pas tenue de mettre à jour les renseignements contenus dans le présent document. Ces renseignements ne peuvent pas remplacer votre propre jugement. Veuillez lire le prospectus avant d'investir.

Des commissions, des commissions de suivi, des frais de gestion et des dépenses peuvent être associés aux placements dans les fonds négociés en bourse (FNB). Veuillez lire le prospectus avant d'investir. Les FNB ne sont pas garantis, leur valeur fluctue fréquemment et le rendement passé ne garantit pas le rendement futur.

Les renseignements contenus dans ce document ont été publiés à une date précise. Bien qu'elles soient considérées comme exactes et fiables au moment de leur publication, nous ne pouvons garantir leur exhaustivité ni leur actualité en tout temps. Certaines déclarations contenues dans ce document constituent des renseignements prospectifs au sens des lois canadiennes sur les valeurs mobilières. Ces renseignements prospectifs peuvent porter sur des éléments divulgués dans ce document et sur d'autres éléments mentionnés dans les documents publics relatifs aux fonds, sur les perspectives d'avenir des fonds et sur les événements ou résultats anticipés, et peuvent inclure des déclarations concernant le rendement financier futur des fonds. Dans certains cas, les informations prospectives peuvent être identifiées par des termes comme « peut », « pourrait », « devrait », « s'attend à », « prévoit », « anticipe », « croit », « a l'intention de », « estime », « prédit », « potentiel », « continue » ou d'autres expressions similaires concernant des éléments qui ne constituent pas des faits historiques. Les résultats réels peuvent différer de ces informations prospectives. Les investisseurs ne devraient pas se fier indûment aux déclarations prospectives. Ces déclarations prospectives sont faites à la date des présentes et nous n'assumons aucune obligation de les mettre à jour ou de les réviser pour tenir compte de nouveaux événements ou circonstances.