Fund in focus: Brompton Split Corp. Enhanced Equity Income ETF.

Global equity markets reacted negatively to the uncertainty and economic disruption caused by the Iran War in March 2026. In April, markets seemed to settle and begin to recover as a fragile ceasefire took hold.

Market turmoil often brings opportunity, and in our view, Brompton Split Corp. Enhanced Equity Income ETF (Ticker: CLSA) looks particularly appealing. CLSA’s portfolio of Split Corp. Class A shares was trading at an average 6.7% discount1 to Net Asset Value (“NAV”) as of April 15, 2026. Class A discounts greater than 5% have historically been a “buy” signal for Class A shares, and in many cases have been followed by periods of outsized performance (see analysis below).

What are Class A Shares?

Class A shares are issued by Split Corps, a unique type of Canadian investment fund. Brompton launched its first split corps over 20 years ago and currently manages seven Toronto Stock Exchange (“TSX”) -listed Split Corps. Split Corps invest in portfolios of high-quality common equities, generally with some form of dividend income which can be split apart from the capital appreciation. Split corps can hold blue chip investments like banks, lifecos, or other categories of dividend-paying shares. Due to Split Corps’ unique capital structure, Class A shares enjoy structural leverage, and so they have enhanced exposure to the performance of the Split Corp’s common share portfolio. In rising markets, Class A shares can provide accelerated returns to investors.

Class A Bargain Hunting Can Deliver Profits

Based on the historical data (for the period from January 2020 to March 2026) from the four Brompton’s longest-tenured Split Corp. Class A shares, Class A shares have generally traded in the market at prices slightly above NAV, representing a premium to NAV. Sometimes, Class A shares trade below NAV, referred to as a discount to NAV. A Class A share which is trading at a 5% discount can be viewed as an opportunity to buy $1.00 worth of NAV for $0.95. In our view, this is a particularly attractive entry point.

Buying Class A shares at discounts to NAV has historically been a profitable investment strategy, often resulting in strong 1-year performance. The table below shows the 1-year performance of four Brompton Split Corp. Class A shares after they have traded at attractive discounts to NAV from January 1, 2010 to March 31, 2025:

Source: Brompton Funds, LSEG Workspace as of March 31, 2026. 1- Yr Return for individual Class A shares are an average of 1-year market price total returns (January 1, 2010 to March 31, 2026) for periods where the discount to NAV is equal or more than 5% and 10% (January 1, 2010 to March 31 2025). Median Class A Premium from January 1, 2010 to March 31, 2025.

One reason why discount trading has been a reliable “buy signal” may be because of the market situation which gives rise to Class A discounts to NAV. One such scenario is when an equity market selloff reaches a bottom and equities start to recover, but potential buyers of Class A shares don’t react quickly enough to the change in NAV for Class A shares. The NAV of a Class A share rises much faster than the underlying stocks they hold, because of the structural leverage provided by the preferred shares, and at times this leveraged increase in the Class A NAV is misunderstood or mispriced in the market. When the Class A NAVs rise faster than the Class A market prices, this creates a discount; and astute investors who buy on the 5%+ discount signal are often rewarded with accelerated returns.

Not Repeating, but Rhyming?

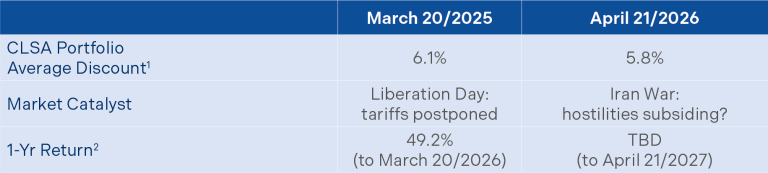

On March 20, 2025, Brompton listed CLSA to give investors a low-cost, diversified way to invest in a variety of Split Corp. Class A shares. At that time, CLSA’s portfolio of Class A shares traded at a 6.1%1 discount to NAV, an attractive level. The markets then went through turmoil as U.S. President Trump announced heavy “Liberation Day” tariffs on global trading partners. Then, the catalyst: tariffs were postponed or lowered. Equity markets rallied, and CLSA powered higher, ending its first year with a 49.2% return.

The current equity market seems oddly similar to March 2025, including a CLSA portfolio trading at attractive discounts to NAV, and a potential catalyst for equity markets:

Conclusion

While buying at a discount is never a guarantee of future performance, CLSA portfolio’s 5.8%1 discount as at April 21, 2026 is a strong signal for Class A investors that believe equity markets will continue to improve over 2026. Buying anything at a discount to intrinsic value is also a measure of downside protection in the event that markets weaken for that asset class. For investors who missed CLSA’s first year’s strong performance after listing, the current market environment and the attractive average discount to NAV of CLSA’s portfolio may provide an attractive entry point.

Returns are for the periods ended March 31, 2026 and are unaudited. Inception date March 20, 2025. The table shows CLSA’s compound return for each period indicated. The performance information shown is based on net asset value per unit and assumes that cash distributions made by CLSA during the periods shown were reinvested at net asset value per unit in additional units of CLSA. Past performance does not necessarily indicate how CLSA will perform in the future.

1 Source: LSEG Workspace and Brompton Funds

2 Source: Morningstar Direct, total return from March 20, 2025 to March 20, 2026.

This document is for information purposes only and does not constitute an offer to sell or a solicitation to buy the securities referred to herein. The opinions contained in this report are solely those of Brompton Funds Limited (“BFL”) and are subject to change without notice. BFL makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, BFL assumes no responsibility for any losses or damages, whether direct or indirect which arise from the use of this information. BFL is under no obligation to update the information contained herein. The information should not be regarded as a substitute for the exercise of your own judgment. Please read the prospectus or annual information form before investing.

Commissions, trailing commissions, management fees and expenses all may be associated with exchange-traded fund investments. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns. Please read the prospectus before investing. Exchange-traded funds are not guaranteed, their values change frequently and past performance may not be repeated.

You will usually pay brokerage fees to your dealer if you purchase or sell shares or units of an investment fund on the Toronto Stock Exchange or other alternative Canadian trading system (an “exchange”). If the shares or units are purchased or sold on an exchange, investors may pay more than the current net asset value when buying shares or units of the investment fund and may receive less than the current net asset value when selling them.

There are ongoing fees and expenses associated with owning shares or units of an investment fund. An investment fund must prepare disclosure documents that contain key information about the fund. You can find more detailed information about the fund in the public filings available at www.sedarplus.ca. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Information contained on this page was published at a specific point in time. Upon publication, it is believed to be accurate and reliable, however, we cannot guarantee that it is complete or current at all times. Certain statements contained in this document constitute forward-looking information within the meaning of Canadian securities laws. Forward-looking information may relate to matters disclosed in this document and to other matters identified in public filings relating to the funds, to the future outlook of the funds and anticipated events or results and may include statements regarding the future financial performance of the funds. In some cases, forward-looking information can be identified by terms such as “may”, “will”, “should”, “expect”, “plan”, “anticipate”, “believe”, “intend”, “estimate”, “predict”, “potential”, “continue” or other similar expressions concerning matters that are not historical facts. Actual results may vary from such forward-looking information. Investors should not place undue reliance on forward-looking statements. These forward-looking statements are made as of the date hereof and we assume no obligation to update or revise them to reflect new events or circumstances.