In our May 2023 Brompton Insights publication on Senior Loans, we highlighted the potential for Senior Loans to deliver equity-like returns given their high current yield and the opportunity for discounted loan prices to return to par. Year-to-date, Loans have returned 9.9% and have continued to outperform high yield bonds (4.7%) and investment grade corporate bonds (-1.4%).1 With the Fed expected to keep rates at an elevated level into 2024, the loan market will continue to benefit from higher yields, setting up a supportive backdrop for returns.

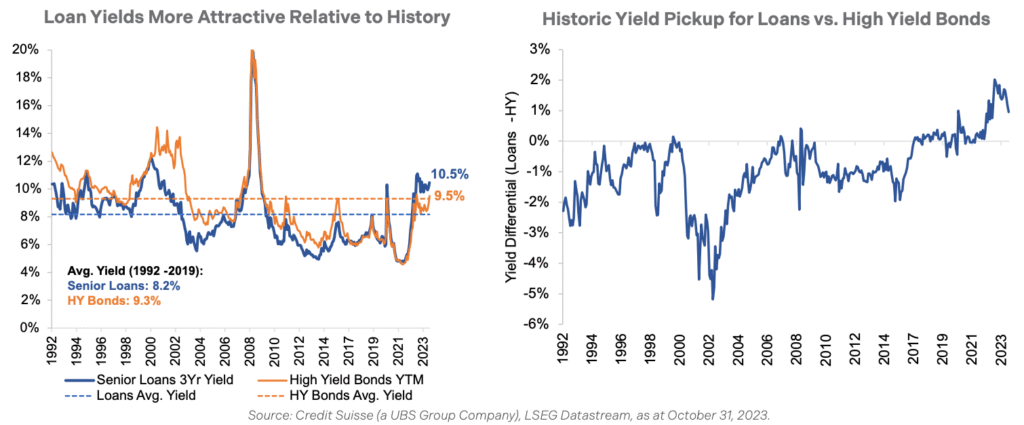

Today, the yield-to-maturity of the Senior Loan Index is 10.5% with a cash yield of 9.8%.2 This continues to imply a forward return profile for Loans that is similar to long-term equity return expectations. Senior Loan yields are currently +228 basis points (bps) higher than their pre-COVID average, while High Yield bond yields have returned to their average level.1 In addition, Loans currently offer a historic yield pick-up relative to High Yield bonds as the differential between Loan and High Yield bond yields is close to the highest it has been since the inception of the Senior Loan Index in 1992.3

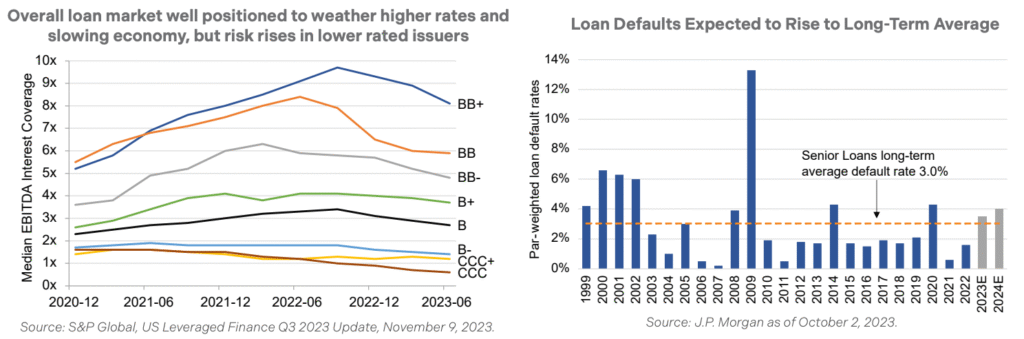

Higher financing costs pose a challenge for borrowers, however a resilient U.S. economy has so far helped borrowers weather the impact. A number of refinancings this year have significantly reduced near-term maturities in 2024 and 2025, which is positive for fundamentals as a lower number of near-term maturities should limit the need for most borrowers to access capital in a potentially tighter credit environment.4 Interest coverage levels for higher-rated loans are generally strong, but lower-quality borrowers face greater risk from higher debt payments, as shown in the chart below (left). According to J.P. Morgan, the average default rate for loans is forecasted to be 3.5% in 2023 and rise to 4.0% in 2024, slightly higher than the long-term average default rate of 3.0%, as shown in the chart below (right). However, loans appear to already be pricing in a meaningful amount of default risk. Conservatively, assuming 50% of defaulted loans are recovered, the discount in the market today with Loans priced at 95% of par value, implies a 10% cumulative default rate. Only in the Great Financial Crisis of 2009, did actual defaults rates get to double digit figures over the past 25 years, so current market pricing is somewhat disconnected from historical default averages.

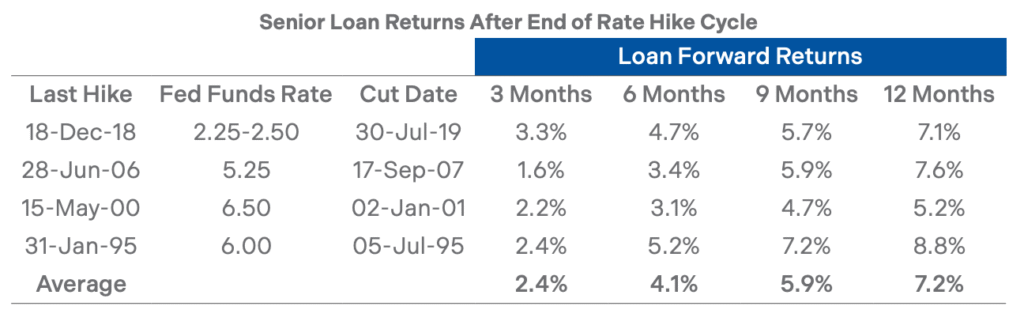

An easing in the U.S. inflation rate in October has increased expectations that the Federal Reserve is done raising rates. Historically, Senior Loan performance has been strong following the start of the pause phase, as shown in the chart below. In the last 30 years, there were four times when the FOMC paused rate increases, and pauses lasted about nine months on average before a rate cut. At the end of the June 2006 rate hiking cycle, the Federal funds rate peaked at 5.25%, a similar level to the current 5.25%-5.50% range. In the twelve months following, Loans returned 7.6%. Since the Loan Index was trading at 99% of par at the time of the pause, this return was comprised primarily of coupon income. Today, the average coupon rate on Loans is 9.2% (1.5% higher than it was in June 2006) with loans priced at 95% of par, offering the potential for additional upside from a return to par from current price levels.2

Senior Loans continue to offer a very attractive level of income for investors. In a higher-for-longer rate environment, the loan market should continue to benefit from higher yields with the potential to deliver equitylike returns. Even if a recession materializes, high current yields provide a meaningful cushion to offset price declines and careful credit selection through active management can help manage risk.

Symphony Floating Rate Senior Loan Fund (SSF.UN) invests in an actively managed, diversified portfolio consisting primarily of Senior Loans and other senior debt obligations of North American non-investment grade corporate borrowers. Nuveen Asset Management LLC, sub-advisor to the fund, specializes in the management of debt and equity strategies including senior loan portfolios, with a 40+ investment professional team dedicated to leveraged finance.

1. Source: Credit Suisse (a UBS Group Company), LSEG Datastream, as at October 31, 2023. Senior Loans: Credit Suisse Leveraged Loan Index, High Yield Bonds: ICE BofA US High Yield Index, Investment Grade Bonds: ICE BofA US Corporate Index.

2. Source: Credit Suisse (a UBS Group Company), as at October 31, 2023. Loans are represented by the Credit Suisse Leveraged Loan Index.

3. Source: Credit Suisse (a UBS Group Company), LSEG Datastream, as at October 31, 2023. Senior Loans: Credit Suisse Leveraged Loan Index, High Yield Bonds: ICE BofA US High Yield Index

4. Source: S&P Global, US Leveraged Finance Q3 2023 Update, November 9, 2023

This document is for information purposes only and does not constitute an offer to sell or a solicitation to buy the securities referred to herein. The opinions contained in this report are solely those of Brompton Funds Limited (“BFL”) and are subject to change without notice. BFL makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, BFL assumes no responsibility for any losses or damages, whether direct or indirect which arise from the use of this information. BFL is under no obligation to update the information contained herein. The information should not be regarded as a substitute for the exercise of your own judgment. Please read the annual information form before investing.

You will usually pay brokerage fees to your dealer if you purchase or sell units of the investment funds on the Toronto Stock Exchange or other alternative Canadian trading system (an “exchange”). If the units are purchased or sold on an exchange, investors may pay more than the current net asset value when buying units of the investment fund and may receive less than the current net asset value when selling them.

There are ongoing fees and expenses with owning units of an investment fund. An investment fund must prepare disclosure documents that contain key information about the fund. You can find more detailed information about the fund in the public filings available at www.sedar.com. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Information contained in this document was published at a specific point in time. Upon publication, it is believed to be accurate and reliable, however, we cannot guarantee that it is complete or current at all times. Certain statements contained in this document constitute forward-looking information within the meaning of Canadian securities laws. Forward-looking information may relate to matters disclosed in this document and to other matters identified in public filings relating to the fund, to the future outlook of the fund and anticipated events or results and may include statements regarding the future financial performance of the fund. In some cases, forward-looking information can be identified by terms such as “may”, “will”, “should”, “expect”, “plan”, “anticipate”, “believe”, “intend”, “estimate”, “predict”, “potential”, “continue” or other similar expressions concerning matters that are not historical facts. Actual results may vary from such forward-looking information. Investors should not place undue reliance on forward-looking statements. These forwardlooking statements are made as of the date hereof and we assume no obligation to update or revise them to reflect new events or circumstances.