Senior Loans are commonly known for having floating rate coupons – a feature that can help limit interest rate risk and provide for higher income in a rising rate environment. However, many investors may not realize that Senior Loans may help mitigate volatility across various market environments. Additionally, current yields and prices for Senior Loans imply total return potential that is comparable to long-term equity return expectations, presenting a compelling risk-reward opportunity for investors looking forward.

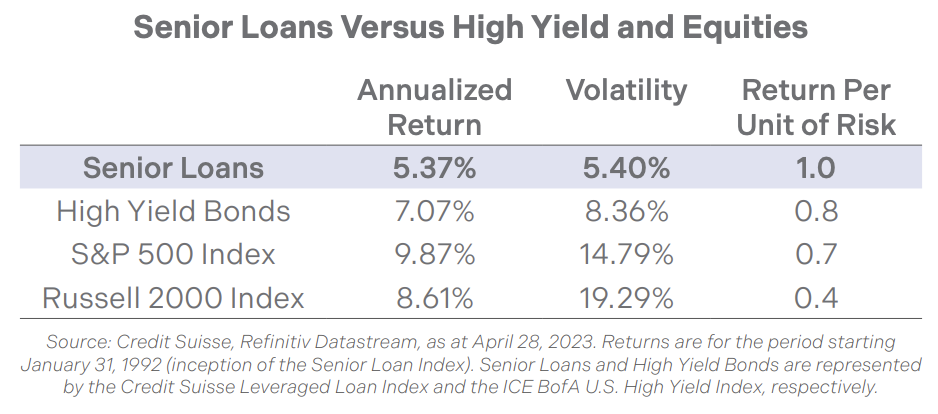

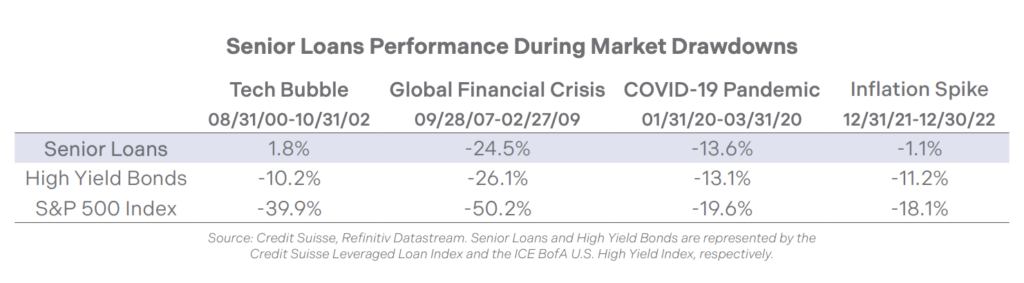

Senior Loans rank senior in the capital structure of a company and are secured by assets, meaning they have the highest priority claim on the pledged assets of the borrower in the event of a default. This protective feature has historically contributed to higher recoveries for investors. The average recovery rate for loans in default has averaged 64% compared with 40% for high yield bonds, according to J.P. Morgan.1 A combination of seniority, security, and low duration has led to loans being a resilient asset class historically, with lower volatility, lower drawdowns and higher risk-adjusted returns compared to high yield bonds and equities, as shown in the charts below.

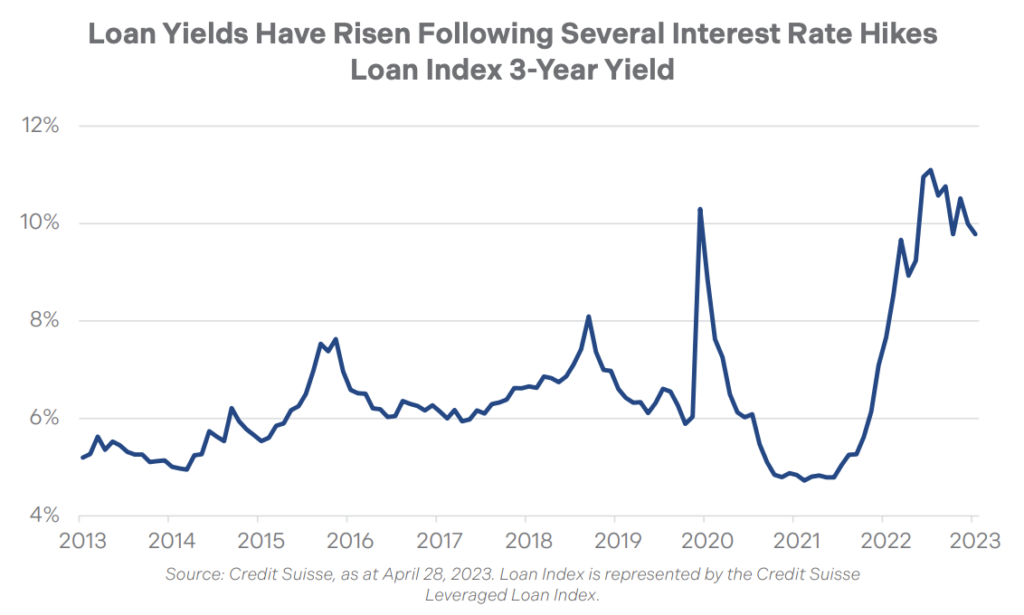

The total return opportunity in loans is driven by two factors. First is the income component which has trended higher with rising interest rates. Today, loans offer a current yield of 9.2% on average, which on its own is attractive, not only relative to historical levels but also relative to the level of yield that can be earned in other asset classes.2 The second source of potential return is from loan prices returning to par value. The average price of loans is currently 93% of par, creating the potential for capital appreciation in addition to the income.2 The current price and spread level for the Senior Loan Index implies a total return opportunity of close to 10%, assuming the discount is amortized over three years, as shown in the chart below.

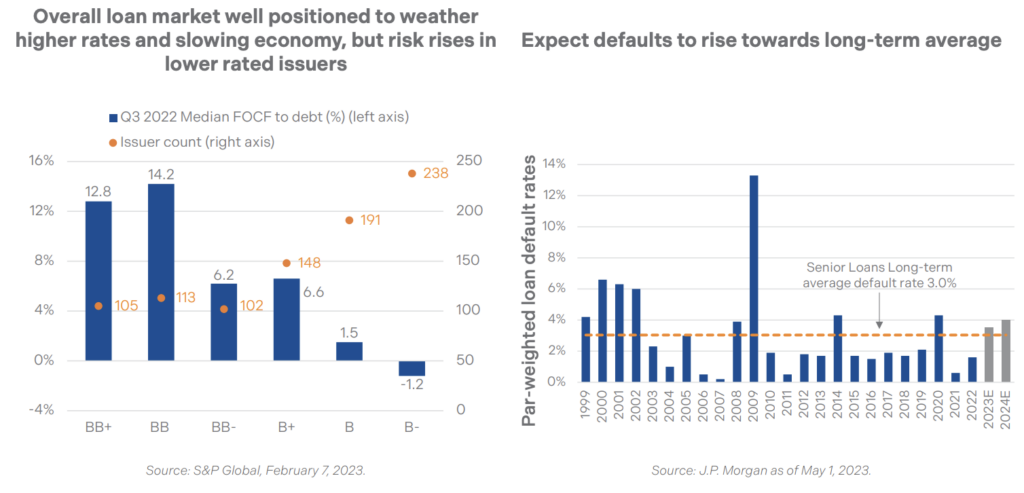

The fundamental backdrop for loans and credit risk assets broadly may become more challenging as higher financing costs and a slowing economy weigh on issuers’ profitability. However, the loan market overall appears well positioned to weather this risk. Interest coverage levels, particularly for higher-rated loans, are generally strong, as shown in the chart below (left) and a low number of near-term maturities should limit the need for most borrowers to access capital in a potentially tighter credit environment. U.S.$54.5 billion of loans are expected to mature by the end of 2024, which represents less than 4% of the loan market.3 While defaults are expected to rise, they are coming off near historic lows and are expected to rise towards longterm average levels. According to J.P. Morgan, the average default rate for loans is forecasted to be 3.5% in 2023 and 4.0% in 2024, as shown in the chart below (right). Loans appear to already be pricing in a meaningful amount of default risk. Conservatively assuming 50% of defaults are recovered, the discount in the market today implies a 14% cumulative default rate.

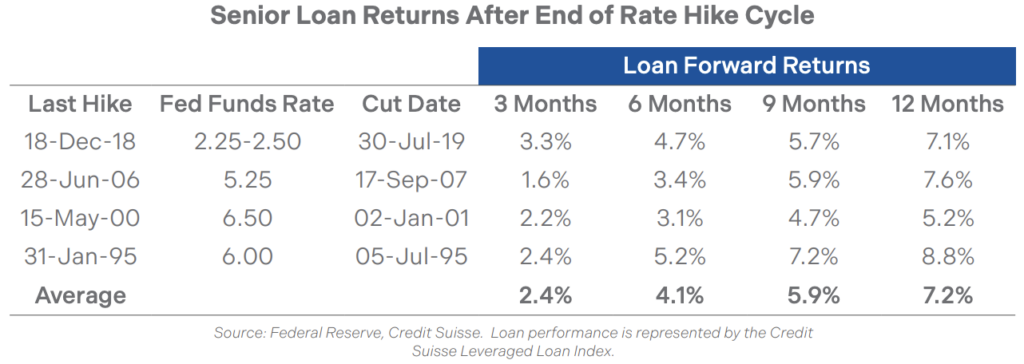

At the May policy meeting, U.S. Federal Reserve Chair Jerome Powell hinted that the FOMC may be ready to end its rate hiking cycle. Historically, Senior Loan performance has been strong following the start of the pause phase, as shown in the chart below. In the last 30 years there were four times when the FOMC paused rate increases, and pauses lasted about nine months on average before a rate cut. At the end of the June 2006 rate hiking cycle, the Federal funds rate peaked at 5.25%, in line with today’s rate. In the twelve months following, Loans returned 7.6%. Since the Loan Index was trading at 99% of par at the time of the pause, this return was comprised primarily coupon income. Today, Loans offer the potential for additional upside from a return to par from current price levels.

While uncertainty around the future path of inflation, interest rates and economic growth poses some challenges for investors, we believe the high current yields and defensive features of Senior Loans can provide a cushion against potential market declines and barring a deep and prolonged recession, Senior Loans can offer an attractive total return opportunity through a combination of high income and price appreciation.

Fund in Focus: Symphony Floating Rate Senior Loan Fund (SSF.UN)

1 Source: J.P. Morgan, as at May 1, 2023. Reflects the 25-year average issuer-weighted recovery rate.

2. Source: Credit Suisse, as at April 28, 2023. Based on the Credit Suisse Leveraged Loan Index.

3. Source: PitchBook LCD; Morningstar LSTA US Leveraged Loan Index, as at March 24, 2023.

This document is for information purposes only and does not constitute an offer to sell or a solicitation to buy the securities referred to herein. The opinions contained in this report are solely those of Brompton Funds Limited (“BFL”) and are subject to change without notice. BFL makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, BFL assumes no responsibility for any losses or damages, whether direct or indirect which arise from the use of this information. BFL is under no obligation to update the information contained herein. The information should not be regarded as a substitute for the exercise of your own judgment. Please read the annual information form before investing.

You will usually pay brokerage fees to your dealer if you purchase or sell units of the investment funds on the Toronto Stock Exchange or other alternative Canadian trading system (an “exchange”). If the units are purchased or sold on an exchange, investors may pay more than the current net asset value when buying units of the investment fund and may receive less than the current net asset value when selling them.

There are ongoing fees and expenses with owning units of an investment fund. An investment fund must prepare disclosure documents that contain key information about the fund. You can find more detailed information about the fund in the public filings available at www.sedar.com. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Information contained on this page was published at a specific point in time. Upon publication, it is believed to be accurate and reliable, however, we cannot guarantee that it is complete or current at all times. Certain statements contained in this document constitute forward-looking information within the meaning of Canadian securities laws. Forward-looking information may relate to matters disclosed in this document and to other matters identified in public filings relating to the funds, to the future outlook of the funds and anticipated events or results and may include statements regarding the future financial performance of the funds. In some cases, forward-looking information can be identified by terms such as “may”, “will”, “should”, “expect”, “plan”, “anticipate”, “believe”, “intend”, “estimate”, “predict”, “potential”, “continue” or other similar expressions concerning matters that are not historical facts. Actual results may vary from such forward-looking information. Investors should not place undue reliance on forward-looking statements. These forwardlooking statements are made as of the date hereof and we assume no obligation to update or revise them to reflect new events or circumstances.